The Picks and Shovels of the AI Era

Inside the infrastructure sectors that have defined the AI investment landscape since ChatGPT's launch, and how sector leadership has rotated as the buildout has evolved.

Sanjeev Pati, CFA

Founder, Scatterplot

TL;DR: Key Takeaways

- The companies powering the AI buildout are not new. Many are decades-old industrial businesses with deep domain expertise. The AI infrastructure story and the AI technology story are two distinct aspects of the same buildout.

- We analyze six AI infrastructure sectors (compute, servers, memory, networking, power, and cooling) by creating an equal-weighted index of publicly traded U.S. equity names in each category.

- All six sectors have significantly outperformed the S&P 500 since January 2023, returning between 4x and 30x the S&P 500's return over the same period.

- Sector leadership has rotated over time, beginning with AI Compute at ChatGPT's launch, moving through Cooling, Power, and Networking, and now sitting firmly with AI Memory & Storage, which has delivered the largest cumulative returns of any category in this analysis.

- Memory was the last sector the market recognized, and has been the most rewarding since.

Introduction

The term "picks and shovels" is often used to describe the AI infrastructure companies building the backbone of the AI era. The phrase itself comes from the California Gold Rush of 1849, where the merchants selling picks and shovels to the miners often did better than the miners themselves. Looking at the picks and shovels of the AI gold rush era so far, that analogy holds up well. The AI companies building large language models may see their profitability play out over years or decades. The infrastructure companies enabling them have, by the numbers, already reaped significant benefits.

It is important to note that, unlike AI itself, the companies building AI infrastructure are not new. These sectors brought decades of hard-won domain expertise to a problem the AI era created at enormous scale and speed. A century-old power company keeping data centers running. A 1960s thermal engineer cooling the world's most powerful chips. A storage business from the PC era feeding data to AI accelerators it was never designed for. One side of this buildout is defined by breakthrough models and novel software. The other is defined by industrial expertise that took decades to build.

It also speaks to something broader, namely the importance of having core industrial expertise within a country, accessible at scale. The most advanced technology in the world still runs on infrastructure that took decades to develop and cannot be replicated overnight.

Methodology

For this analysis, we constructed six equally weighted indices of U.S. stocks representing the AI infrastructure stack, with a start date of January 1, 2023, broadly representing the beginning of the modern AI era following the public launch of ChatGPT in Q4 2022. The six categories are:

AI Compute

AI Servers & Systems

AI Memory & Storage

AI Networking & Optical

AI Power & Energy

AI Cooling & Thermal

All returns are total returns including reinvested dividends. The full list of constituent stocks for each category is included in the Category Deep Dive section below.

The diagram below shows how the six sectors relate to each other within the AI infrastructure stack.

The Full Infrastructure Scorecard

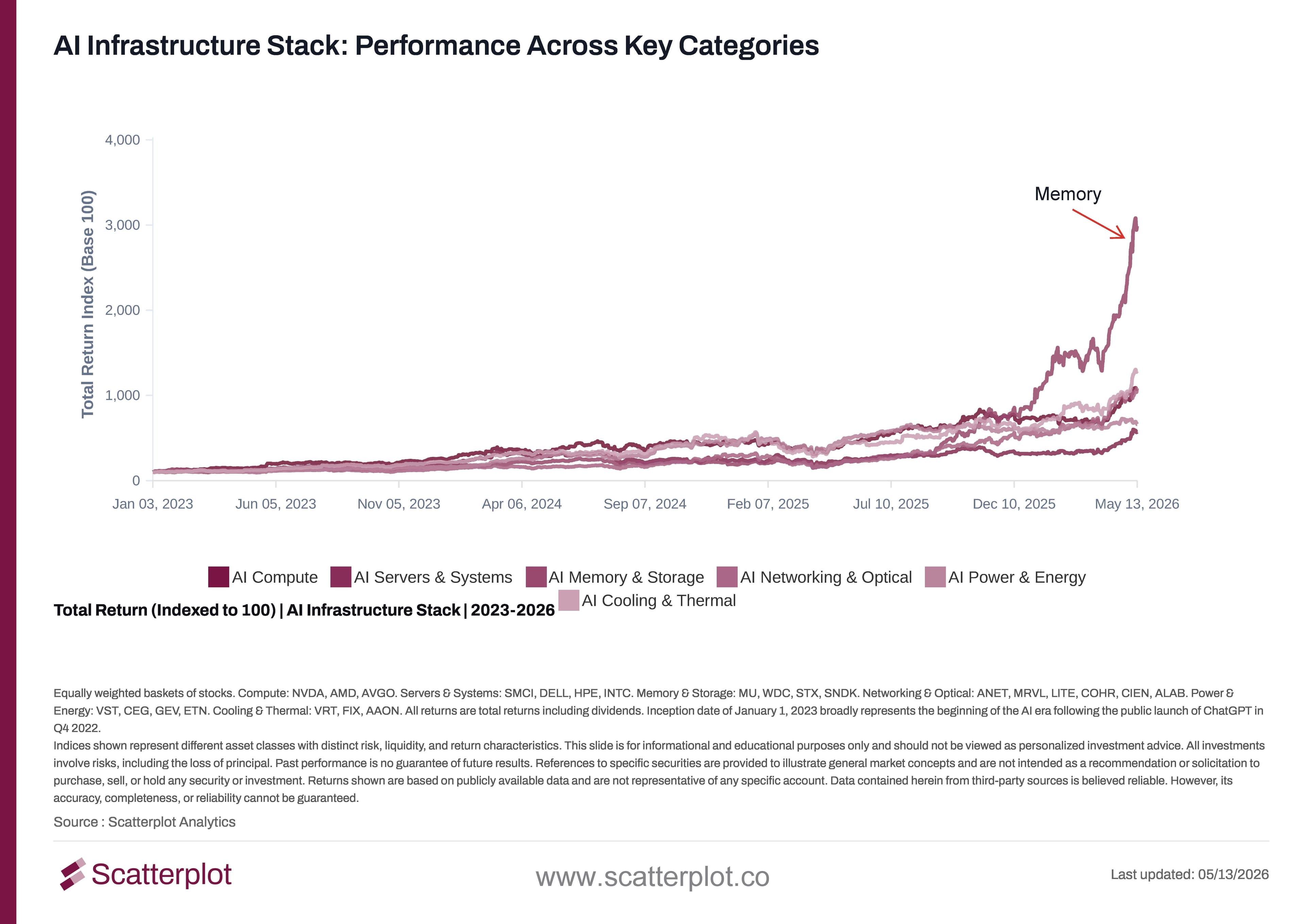

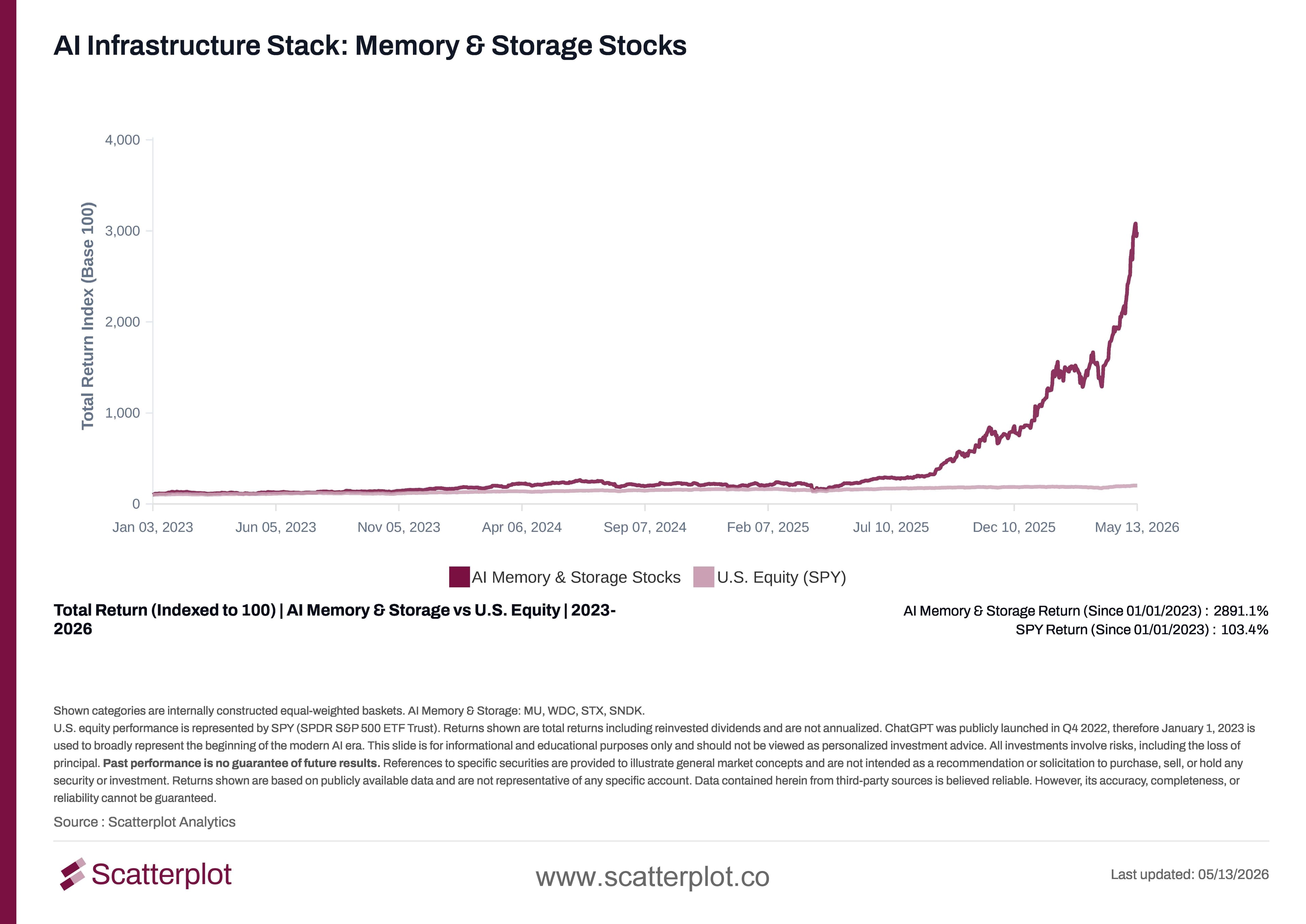

ChatGPT was released in Q4 2022, marking the beginning of the modern AI era. We track returns from January 1, 2023, the first full year of that era, to capture how each infrastructure sector has performed since the buildout began. As the table and chart below make clear, each of these AI infrastructure sectors has significantly outperformed the broader equity market. Even the lowest returning sector. AI Servers & Systems returned approximately 5x the S&P 500's return over this period. AI Memory & Storage came into prominence in the middle of 2025 and has since been the top performing sector, up over 2,800% since January 2023, almost 30x the S&P 500's return, a staggering number even in the context of the extraordinary returns this AI era has produced. The chart below plots the total return of each sector index against the S&P 500 since January 2023, indexed to 100 at the start. The line peaking well above all others is AI Memory & Storage.

This chart updates daily. Track it live at scatterplot.co

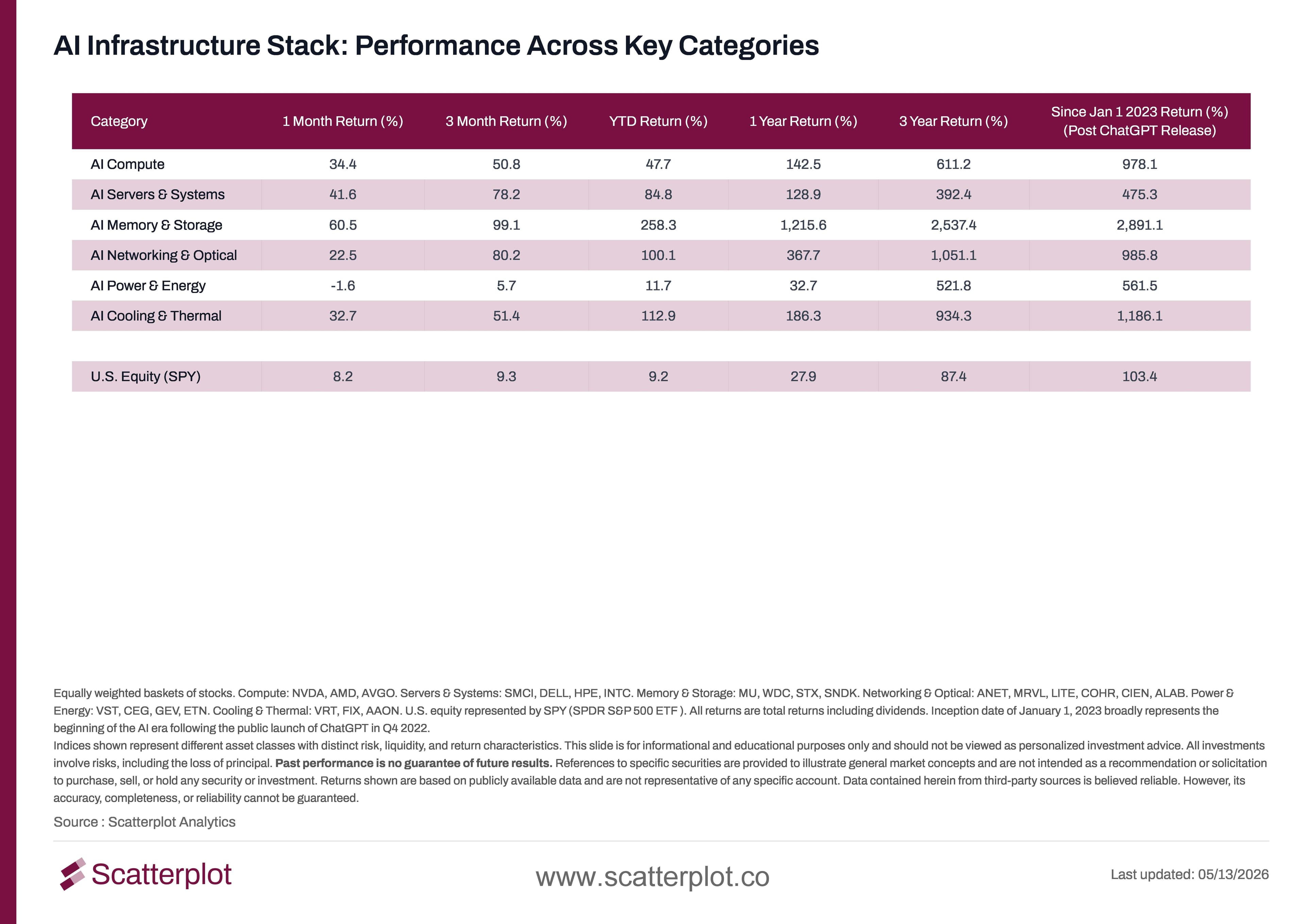

The table below shows the total returns for each category across multiple time periods, from one month to since the launch of ChatGPT.

This chart updates daily. Track it live at scatterplot.co

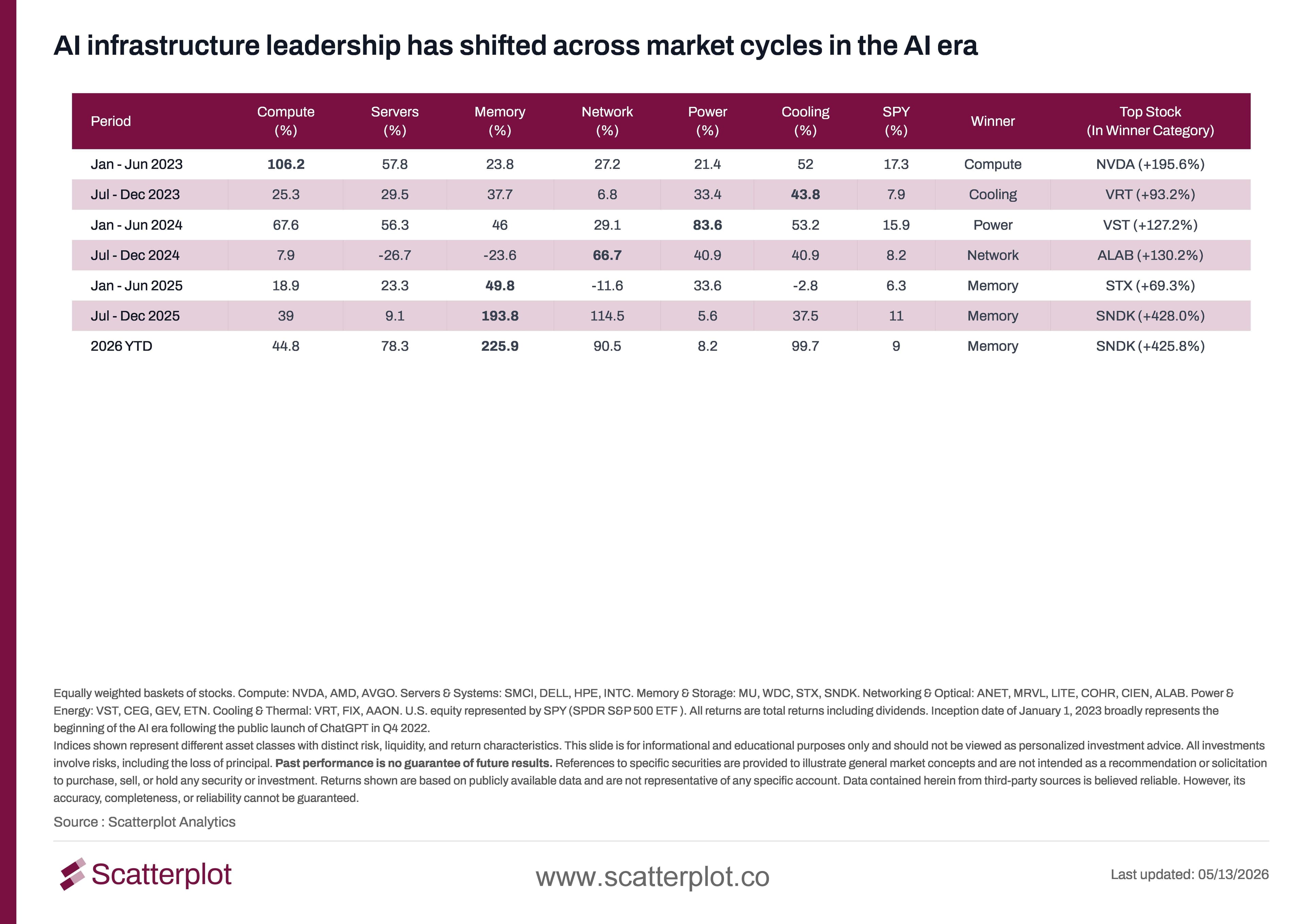

How Leadership Has Rotated: A Half-Year by Half-Year Story

The historical return data across all six sectors has been significant. Narrowing to sector leadership, we see a clear rotation. Different sectors led in the early periods of the buildout, each reflecting a specific bottleneck or constraint the market had begun to price.

Narrowing the lens further, the table below breaks down returns by half-year period, showing which sector led the market at each stage of the AI buildout and the standout stock within it.

This chart updates daily. Track it live at scatterplot.co

The early winner was compute. NVIDIA (NVDA), the dominant AI chip designer, returned approximately 200% in the first half of 2023 (H1 2023). Cooling followed, with Vertiv (VRT), a data center thermal management specialist, being the standout performer in H2 2023, returning approximately 95%. Power came next, with Vistra (VST), an independent power producer, returning approximately 125% in H1 2024. Networking took the lead in H2 2024, with Astera Labs (ALAB), a semiconductor connectivity solutions company, up approximately 130%. And then came memory, a late winner in this cycle, relatively speaking, but the dominant one by a considerable margin for over a year now. SanDisk (SNDK), a pure-play flash storage company, returned approximately 420% in the second half of 2025 and is up over 420% year-to-date in 2026.

Category Deep Dives

The table above tells the performance story. Here is what each sector actually does and the key stocks behind it.

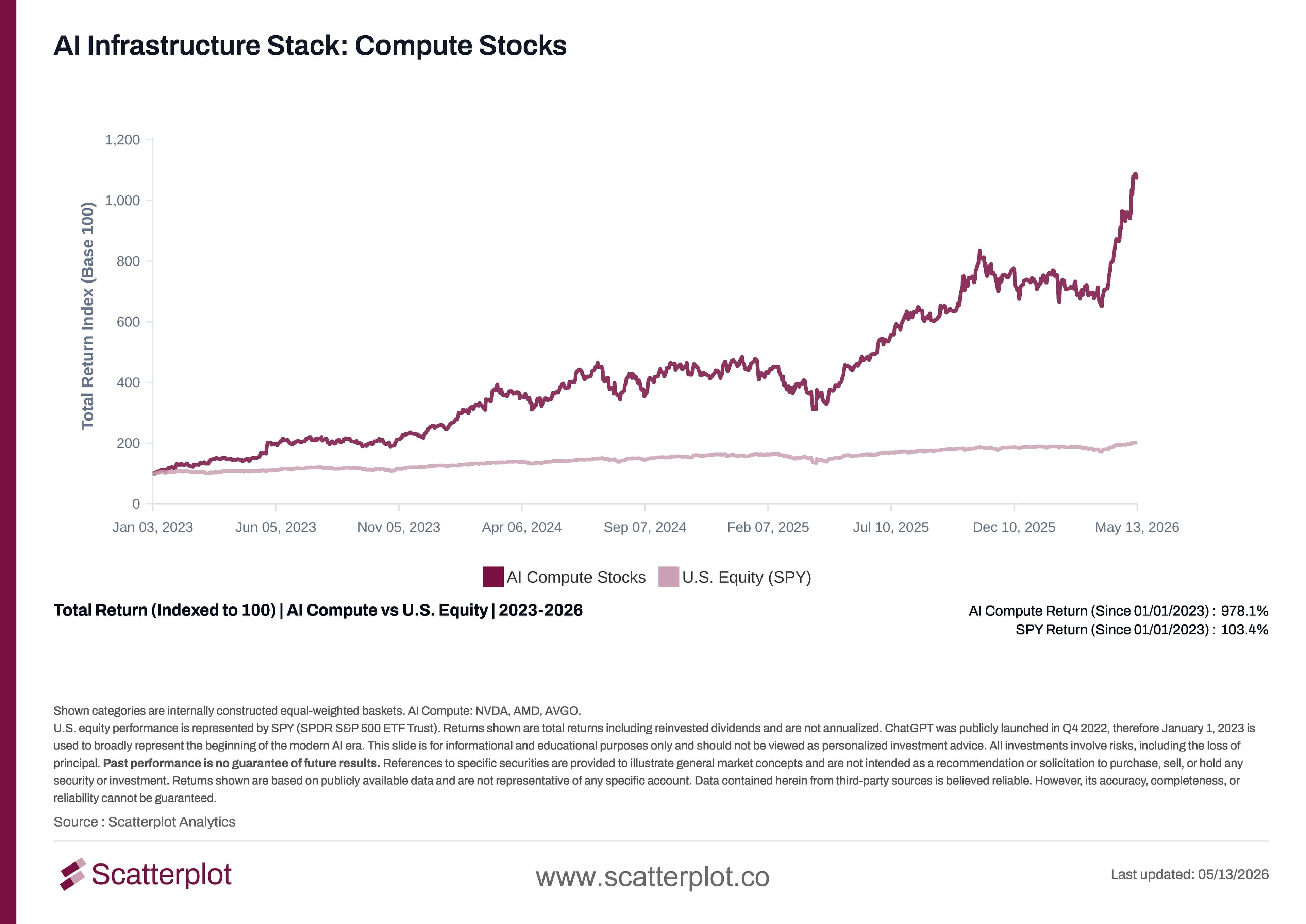

AI Compute

As the chart below shows, AI Compute is where investors went first. The first pick and shovel they picked up. This category has received the most attention but is not the highest returning sector in this analysis. NVIDIA (NVDA) is the name most associated with the AI trade, and for good reason. It returned over 1,400% since January 2023. Advanced Micro Devices (AMD) returned almost 600% and Broadcom (AVGO) almost 700% over the same period. Stocks in this sector, weighted equally to create this index: NVIDIA (NVDA), Advanced Micro Devices (AMD), Broadcom (AVGO). The chart below shows how the AI Compute index has performed against the S&P 500 since January 2023.

This chart updates daily. Track it live at scatterplot.co

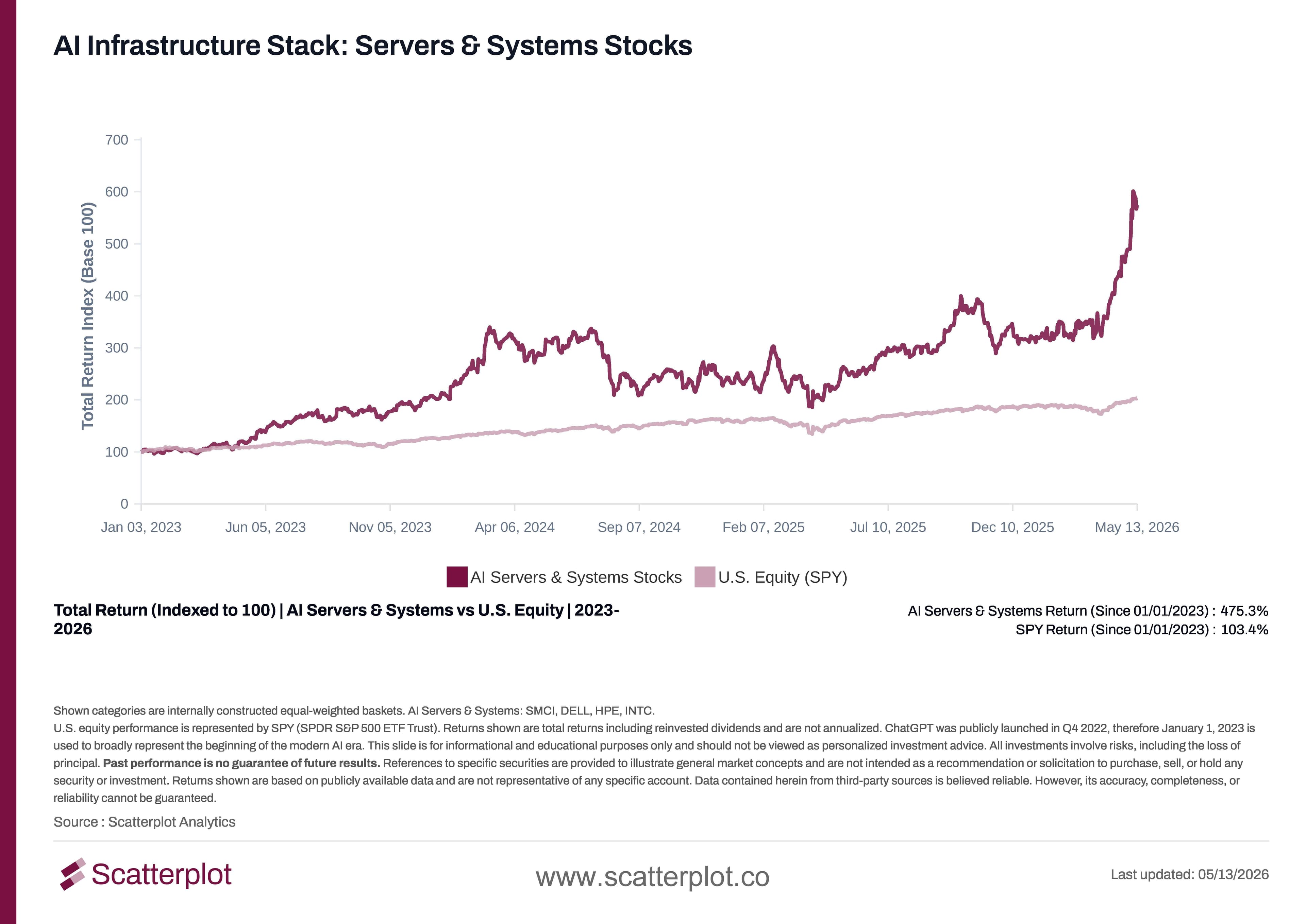

AI Servers & Systems

Like Compute, AI Servers and Systems were recognized early as part of the AI infrastructure buildout, but the companies in this sector took longer to reflect that in their returns. Some, like Super Micro Computer (SMCI) faced company-specific headwinds. Others, like Intel (INTC) and Hewlett Packard Enterprise (HPE), are large, diversified businesses where AI represented one part of a broader portfolio. More recently, the scale of AI capital expenditure has been a significant tailwind for the sector, and as the chart below shows, returns have moved meaningfully higher. Dell Technologies (DELL) returned approximately 530% since January 2023. Intel (INTC) returned over 350%. Hewlett Packard Enterprise (HPE) returned over110%. Super Micro Computer (SMCI) returned approximately 280%. This is also the only sector that never led a single half-year period in the rotation table. Stocks in this sector, weighted equally to create this index: Super Micro Computer (SMCI), Dell Technologies (DELL), Hewlett Packard Enterprise (HPE), Intel (INTC). The chart below shows how the AI Servers & Systems index has performed against the S&P 500 since January 2023.

This chart updates daily. Track it live at scatterplot.co

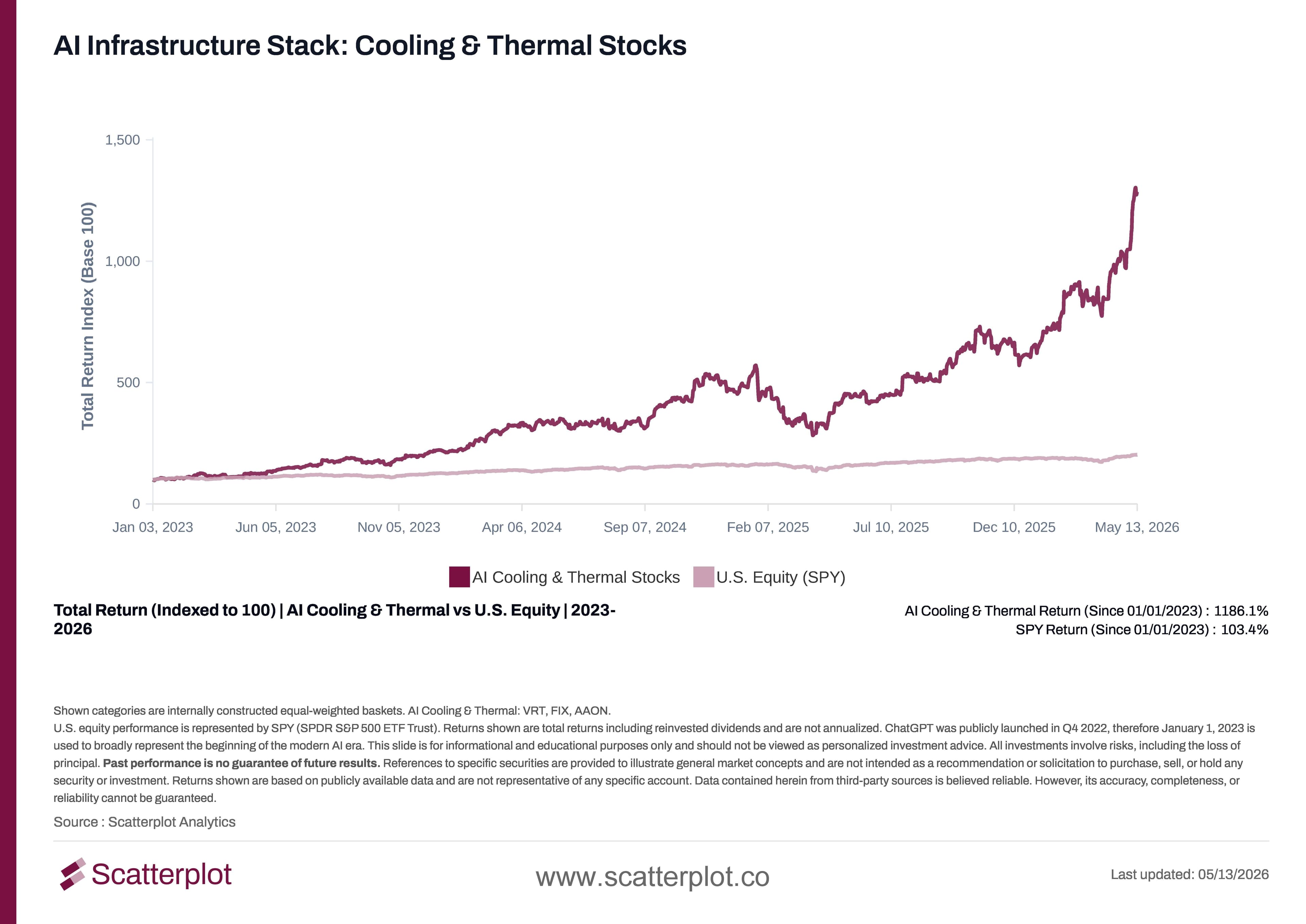

AI Cooling & Thermal

One of the early winners in this analysis. As data center capital expenditure grew, this sector benefitted alongside it, and has seen significant returns since early 2025. Vertiv (VRT), a thermal management company founded in 1965, returned over 2,600% since January 2023, nearly twice NVIDIA's return over the same period. VRT has been the single best performing stock across all six sectors in this analysis, based on the data presented here. Comfort Systems USA (FIX) returned over 1,600%. AAON (AAON) returned approximately 170%. Stocks in this sector, weighted equally to create this index: Vertiv (VRT), Comfort Systems USA (FIX), AAON (AAON). The chart below shows how the AI Cooling & Thermal index has performed against the S&P 500 since January 2023.

This chart updates daily. Track it live at scatterplot.co

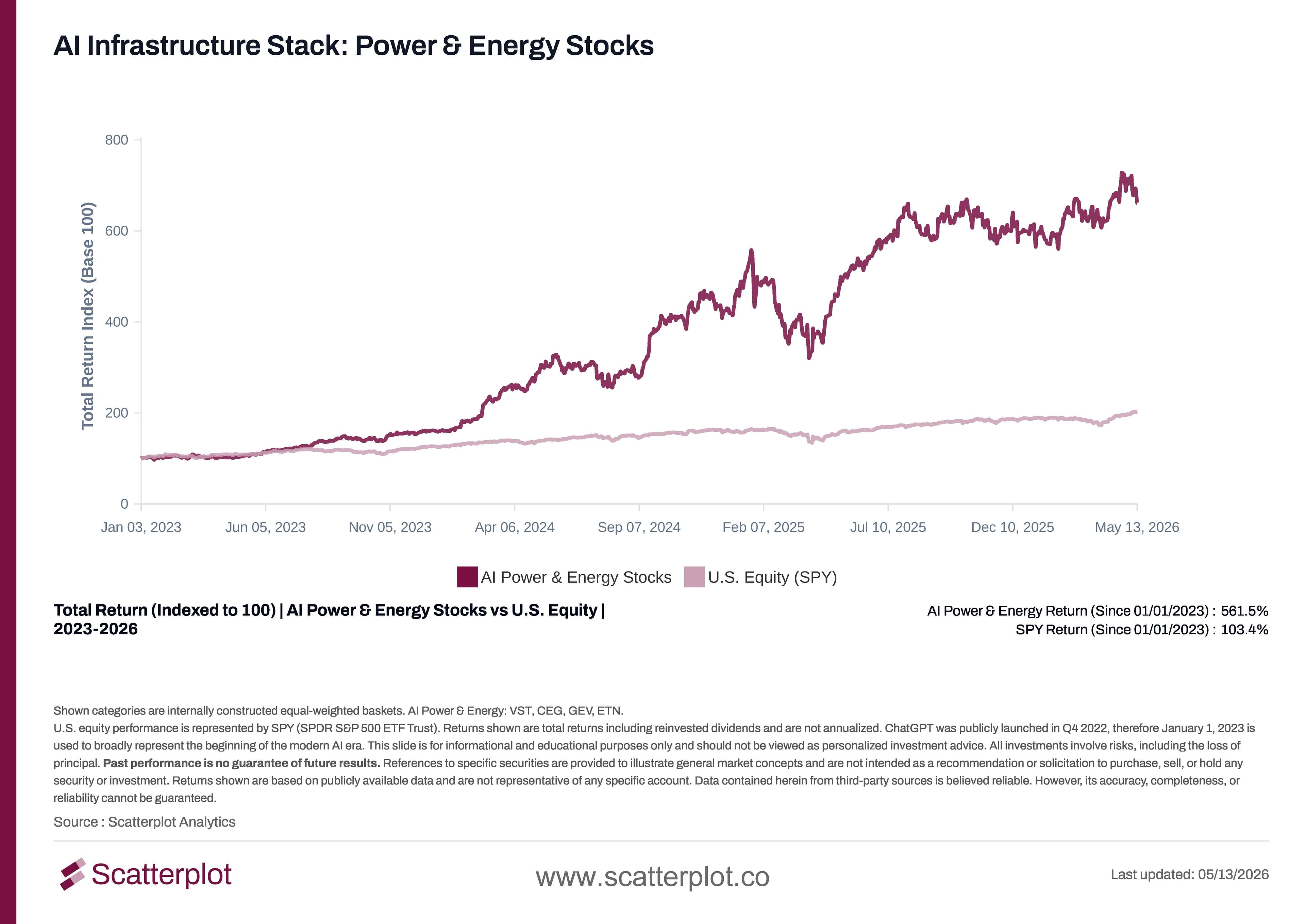

AI Power & Energy

These are among the most traditional companies in this analysis. Vistra (VST) traces its roots to 1882, Eaton (ETN) to 1911, and GE Vernova (GEV) to the industrial heritage of General Electric, founded in 1892. This sector has not seen the parabolic returns of others in recent periods, but it has been an important and consistent part of the AI infrastructure buildout, providing the electricity that every data center, chip, and server ultimately depends on. Vistra (VST) returned about 600% and Constellation Energy (CEG) approximately 250% since January 2023. Eaton (ETN) returned approximately 170%. Stocks in this sector, weighted equally to create this index: Vistra (VST), Constellation Energy (CEG), GE Vernova (GEV), Eaton (ETN). The chart below shows how the AI Power & Energy index has performed against the S&P 500 since January 2023.

This chart updates daily. Track it live at scatterplot.co

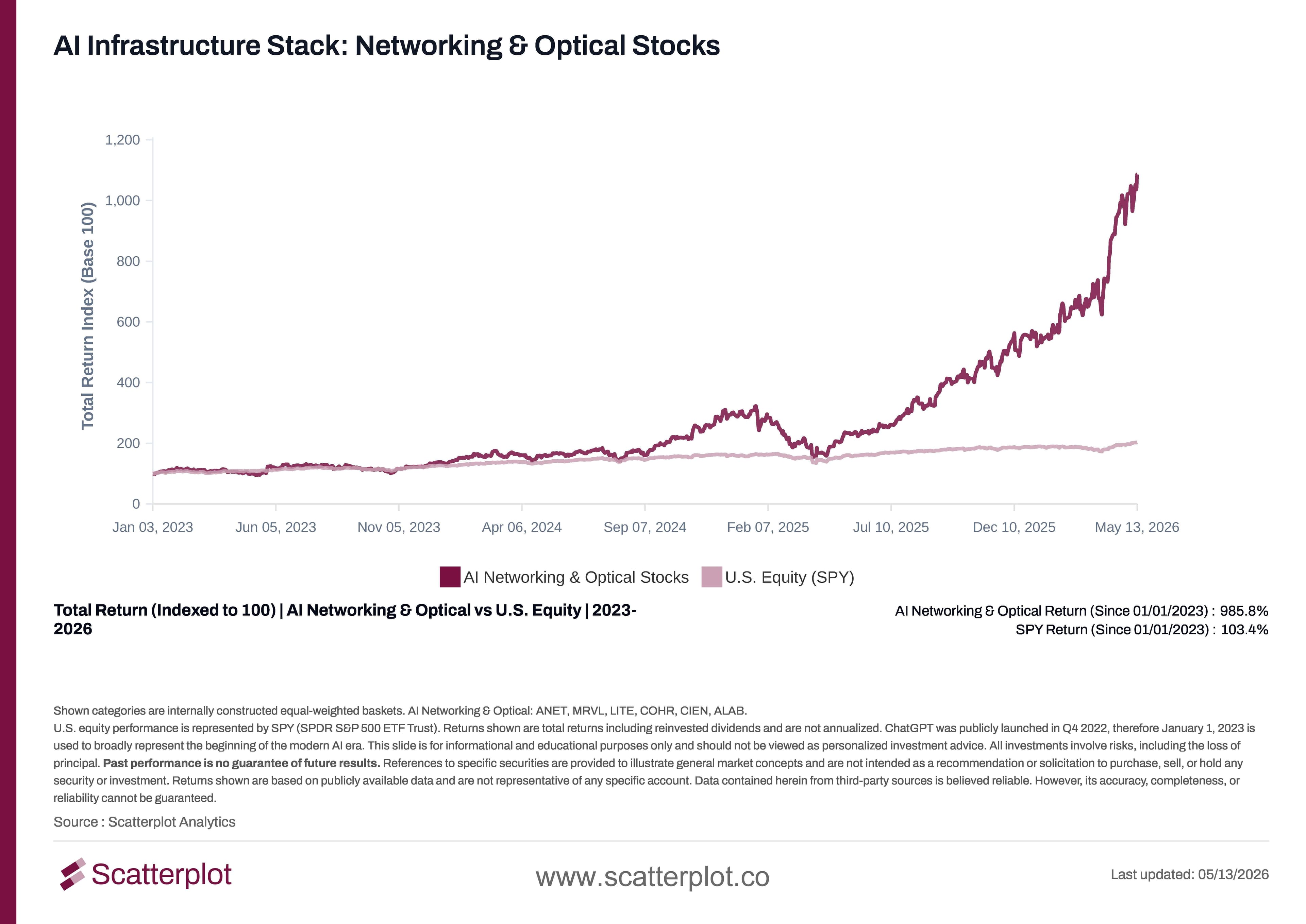

AI Networking & Optical

A late entrant in the AI infrastructure trade, but its historical returns have been significant. Like Memory, 2025 was a breakout year for this sector and it has only moved higher since. As AI clusters scaled, moving data between chips and servers fast enough became a binding constraint, and the market began pricing in the networking buildout in earnest. Lumentum (LITE), an optical components company, returned approximately 1,800% since January 2023, more than NVIDIA. Coherent (COHR) and Ciena (CIEN) over 1,000%. Arista Networks (ANET) returned approximately 350% and Marvell Technology (MRVL) approximately 400%. Stocks in this sector, weighted equally to create this index: Arista Networks (ANET), Marvell Technology (MRVL), Lumentum (LITE), Coherent (COHR), Ciena (CIEN), Astera Labs (ALAB). The chart below shows how the AI Networking & Optical index has performed against the S&P 500 since January 2023.

This chart updates daily. Track it live at scatterplot.co

AI Memory & Storage

The last pick and shovel investors picked up. Memory stocks stayed away from the AI trade until about 12 months ago, and then went on to become the most profitable AI infrastructure trade in this entire analysis. The returns across the constituent stocks have been notable. Seagate Technology (STX), a storage company founded in 1978, returned over 1,600%. Western Digital (WDC) returned almost 2,000%. Micron Technology (MU) returned over 1,500%. SanDisk (SNDK), which spun off from Western Digital mid-cycle, is up almost 420% year-to-date in 2026 alone. Stocks in this sector, weighted equally to create this index: Micron Technology (MU), Western Digital (WDC), Seagate Technology (STX), SanDisk (SNDK). The chart below shows how the AI Memory & Storage index has performed against the S&P 500 since January 2023. The breakout in mid-2025 is clearly visible.

This chart updates daily. Track it live at scatterplot.co

Frequently Asked Questions

What does "picks and shovels" mean in the context of AI?

The phrase comes from the California Gold Rush of 1849, where the merchants selling picks and shovels to miners often did better than the miners themselves. In the context of AI, it refers to the companies supplying the tools and infrastructure that make AI possible, including the chips, servers, power systems, cooling equipment, networking hardware, and memory, rather than the AI software companies themselves. The idea is that regardless of which AI models or applications ultimately win, the infrastructure enabling them all needs to be built regardless.

How are the Scatterplot AI infrastructure indices constructed?

Each index is an equally weighted basket of publicly traded U.S. equities, with a start date of January 1, 2023. Constituents: AI Compute: NVIDIA (NVDA), Advanced Micro Devices (AMD), Broadcom (AVGO). AI Servers & Systems: Super Micro Computer (SMCI), Dell Technologies (DELL), Hewlett Packard Enterprise (HPE), Intel (INTC). AI Memory & Storage: Micron Technology (MU), Western Digital (WDC), Seagate Technology (STX), SanDisk (SNDK). AI Networking & Optical: Arista Networks (ANET), Marvell Technology (MRVL), Lumentum (LITE), Coherent (COHR), Ciena (CIEN), Astera Labs (ALAB). AI Power & Energy: Vistra (VST), Constellation Energy (CEG), GE Vernova (GEV), Eaton (ETN). AI Cooling & Thermal: Vertiv (VRT), Comfort Systems USA (FIX), AAON (AAON). All returns are total returns including reinvested dividends. This analysis is for informational and educational purposes only. Past performance is no guarantee of future results.

How have AI infrastructure stocks performed relative to the S&P 500 since ChatGPT launched?

All six AI infrastructure sectors tracked in this analysis have significantly outperformed the S&P 500 since January 2023, returning between approximately 4x and 30x the S&P 500's return over the same period. The S&P 500 (SPY) returned approximately 103% over this period. AI Servers & Systems was the lowest returning category at approximately 475%, while AI Memory & Storage was the highest at approximately 2,890%. All returns are total returns including dividends and are for informational purposes only. Past performance is no guarantee of future results.

With this fast-moving AI Story, how do we track it?

The charts and data underlying this analysis are updated daily on Scatterplot, making it straightforward to monitor how each sector and individual stock is performing at any given time. The rotation table, scorecard, and individual sector charts are all refreshed on a daily basis, so the picture you see reflects current market data rather than a static snapshot. This analysis is for informational purposes only and is not investment advice.

Conclusion

The data tells a clear story. Since ChatGPT launched, the AI infrastructure buildout has produced some of the most notable equity returns in recent market history. Not just for the companies building the models. For the companies building the pipes, the power lines, the cooling systems, the chips, and the storage that make it all run.

What makes this story particularly striking is the rotation. The market did not price all of this at once. It worked through the stack methodically, sector by sector, as each bottleneck became visible. And the last sector to be recognized, Memory, turned out to be the most rewarding of all.

How the data develops from here is something Scatterplot will continue to track.

Disclosure

This content is for informational and educational purposes only and should not be viewed as personalized investment advice. Indices shown represent different asset classes with distinct risk, liquidity, and return characteristics. All investments involve risks, including the loss of principal. Past performance is no guarantee of future results. References to specific securities are provided to illustrate general market concepts and are not intended as a recommendation or solicitation to purchase, sell, or hold any security or investment. Data contained herein from third-party sources is believed reliable; however, its accuracy, completeness, or reliability cannot be guaranteed.

Enjoyed this? Get more in your inbox.

Weekly insights for advisors

— charts, research, and practical tools. No fluff.

Investment Foundations

Understanding Recency Bias: What U.S. Equity Returns Reveal About Investor Expectations

Exploring Recency Bias in Investors Using Recent and Long-Term U.S. Equity Data.

Read moreSanjeev Pati, CFA

July 6, 2026 · 4 min read

Investment Foundations

Why Market Timing Is So Hard: 70% of the best days in the market land near the worst ones

Market timing is hard. Since 1993, 70% of the S&P 500's ten best trading days occurred within 20 days of one of its ten worst trading days, making it difficult to capture one without being exposed to the other.

Read moreSanjeev Pati, CFA

June 26, 2026 · 5 min read